In early 2015, I wrote about SAFE instruments, which I then had heard about but not yet seen in my practice, with a gently mocking but grudgingly intrigued tone, which likely resulted from the trend having originated on the West Coast. (As a native New Yorker, I have been trained to roll my eyes at each new development from California and then promptly forget about that when I incorporate it into my life.) With over three years of experience with SAFEs in my practice, I thought it appropriate to update my post, less the cynicism, since they have become pretty common and accepted in the world of early stage corporate finance.

A SAFE instrument (Simple Agreement for Future Equity) is an alternative to convertible notes for startups seeking bridge financing to keep the lights on until they can raise substantial funds in a true equity round. Y Combinator offers open source SAFE equity forms with some background information. With a convertible note, the seed investor acts temporarily as a lender, with the note being converted to equity if and when the company completes a qualifying equity financing. With SAFE equity, the investor simply receives the right to receive preferred equity when the qualified financing is completed, without the need to temporarily treat it as a loan. There is no interest, maturity date, repayment terms or any other provisions that you’d associate with a debt instrument.

SAFE promoters correctly point out that these seed investors are not ultimately seeking a debt-like steady return on their investment. As early-stage equity investors, they have more of a high risk/high reward orientation. Convertible notes are usually not repaid in cash. The more likely scenarios are that (1) they are converted into equity, or (2) the company fails to complete a financing and realistically is not able to pay back the note. In the first scenario, the accrued interest adds to the amount of shares issued upon conversion, giving the investors a windfall that they would not have expected by making a simple equity investment. With SAFEs, the investment is treated like an equity instrument, which reflects the intent of both parties.

The SAFE folks also tout the relative simplicity of the SAFE documentation. There is only one five-page document to be executed, and there aren’t a lot of moving parts requiring much customization. Essentially, the parties need to only agree on whether there is a cap on the valuation of the later financing for purposes of determining the number of shares to be issued to the investor, and whether the investor receives a discount on the conversion price when the later financing is completed. In fairness, convertible notes are themselves fairly simple and are used because they are themselves much simpler than VC equity documents, but SAFE equity appropriately combines simplicity with avoiding introducing debt concepts where not intended.

Finally, the absence of a maturity date with SAFEs takes the time pressure off of the company to complete the equity offering within a particular timeline, though investors may prefer having such a deadline in place to incentivize a quick completion of an offering.

Rule 506(c), the provision arising out of the JOBS Act that enables companies to raise capital using general solicitation and advertising while still being exempt from SEC registration requirements, has always had the potential to revolutionize the capital raising process. With the ability of companies to connect easily with potential investors anywhere via the internet and social media, one could imagine a world where this supplants private placements under Rule 506(b), in which the investor base is, by definition, limited based on existing relationships with the company or its broker-dealer. While the use of Rule 506(c) has grown since enactment, it has nowhere near the usage rate of Rule 506(b). In 2017, Rule 506(c) offerings represented only 4% in dollar amount of all Regulation D offerings.

Rule 506(c), the provision arising out of the JOBS Act that enables companies to raise capital using general solicitation and advertising while still being exempt from SEC registration requirements, has always had the potential to revolutionize the capital raising process. With the ability of companies to connect easily with potential investors anywhere via the internet and social media, one could imagine a world where this supplants private placements under Rule 506(b), in which the investor base is, by definition, limited based on existing relationships with the company or its broker-dealer. While the use of Rule 506(c) has grown since enactment, it has nowhere near the usage rate of Rule 506(b). In 2017, Rule 506(c) offerings represented only 4% in dollar amount of all Regulation D offerings.

A recent Wall Street Journal article highlighted how

A recent Wall Street Journal article highlighted how  Offerings") Back when the

Back when the  Matt Levine, writing in Bloomberg View,

Matt Levine, writing in Bloomberg View,

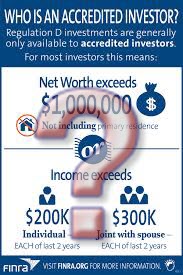

Securities offerings that are exempt from the SEC’s registration requirements often hinge on whether some or all of the investors are “

Securities offerings that are exempt from the SEC’s registration requirements often hinge on whether some or all of the investors are “ On September 5, 2017, the U.S. House of Representatives overwhelmingly approved a bill that would allow already-public reporting companies to use the provisions of so-called Regulation A+ to make securities offerings.

On September 5, 2017, the U.S. House of Representatives overwhelmingly approved a bill that would allow already-public reporting companies to use the provisions of so-called Regulation A+ to make securities offerings.  William D. Cohan, writing in the New York Times’ DealBook, characterizes the

William D. Cohan, writing in the New York Times’ DealBook, characterizes the