The SEC’s SPAC Proposal and Projections

The SEC has issued its long-expected proposed rules regarding SPACs. Here are the proposing rule release and the shorter press release. The SEC has always been skeptical of SPACs, and the rules are generally designed to impose new disclosure requirements on SPACs that make the rules more aligned with those applicable to traditional IPOs. One of the reasons SPACs had their moment in the sun recently is that they are easier to complete than IPOs, so the rules, if enacted, could have the effect of severely dampening the market for SPACs, even if they do nothing to directly restrict them from being done. In fact, the general expectation that rules like these were coming down the pike has, anecdotally, been a factor in the SPAC market slowing down recently.

One of the key areas in the proposed rules relates to projections. Under current rules, companies merging with a SPAC can include projections about the company’s future expected results and can benefit from a safe harbor protecting it from litigation if the projections don’t come to pass, as long as the projections are accompanied by a disclaimer and the companies don’t have actual knowledge that they won’t come true. In contrast, companies going public the traditional way don’t have the benefit of this safe harbor. The proposed rules would eliminate the safe harbor in the SPAC context, which would have the practical effect of precluding most projections from being presented.

…The SEC’s SPAC Proposal and Projections Read More »

As of December 2, 2020,

As of December 2, 2020,  The SEC recently

The SEC recently  Jason Zweig, writing in the Wall Street Journal, discusses

Jason Zweig, writing in the Wall Street Journal, discusses  The SEC has greatly expanded the number of public companies that can take advantage of the “scaled disclosure” provisions of Regulation S-K.

The SEC has greatly expanded the number of public companies that can take advantage of the “scaled disclosure” provisions of Regulation S-K.

A recent Wall Street Journal article highlighted how

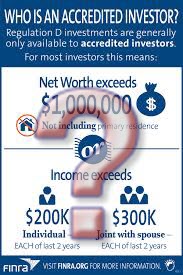

A recent Wall Street Journal article highlighted how  Securities offerings that are exempt from the SEC’s registration requirements often hinge on whether some or all of the investors are “

Securities offerings that are exempt from the SEC’s registration requirements often hinge on whether some or all of the investors are “